Section 1- About GST - Introduction

“GST” needs no new introduction. It is a historic and one of the tax reforms in the post independent India. It is expected to simplify the current indirect taxes regime and make it easier for all businesses to collect and pay taxes.

GST is a presumption-based tax on goods and services. India has opted for a Dual-GST which very few other countries have adopted. Most countries such as Malaysia and Singapore have adopted a single-GST whereby one nation one tax is the principle they have followed. But India being a quasi-federal country where the power to tax is equally divided between states and center, implemented the dual GST. Earlier, the center used to levy tax on services, manufacturing and sale of goods whereas, entry tax power was with the states. Now all these will go away and for taking these states on-board, the center decided to go with a Dual-GST model.

Essentials of Goods and Service Tax

GST is ONE comprehensive levy on all goods and services instead of levying multiple indirect taxes being at various stages of supply chain. GST supplants the current indirect tax regime which is known for its multiplicity of taxes, restricted credit flow, copious legislations, varying threshold limits and umpteen instances of cascading, thereby hindering the growth and competitiveness and adding to the woes of businesses in India.

In order to satiate the unyielding need to facilitate “Ease of Doing Business”, attain higher growth in terms of GDP, making “Make in India” a reality, encourage better tax compliance and to bring about transparency in tax administration, it is but natural for GST to gain the astounding momentum that it has in the last few months.

The dual GST which would be implemented in India is a destination-based value added tax, levied at all points in the supply chain with credit allowed for tax paid on purchases used in making the supply. It would apply to both goods and services in a comprehensive manner with exemptions restricted to bare minimum.

Karvy GST – Going Digital for GST compliance

In line with becoming digital India GST is a step moving from an era of cumbersome paper-based compliance system to a tech-savvy paper less compliance and administration model.

The Goods and Service Tax Network (“GSTN”) forms the IT backbone of the GST system. It is going to be a shared IT platform for both central and state governments. The GST System is going to have a G2B portal, implying tax payers will have to access and interface with the GST systems directly. However, tax payers' convenience will be a key factor in success of GST regime. As a measure to achieve the same, the tax payers may interact with the GSTN through a third party service provider generically known as “GST Suvidha Providers (GSP)”.

Section 2 – Karvy as GST Suvidha Provider

The GSTN

Goods and Services Tax Network (GSTN) is a Section 8 (under new companies Act, not for profit companies that are governed under section 8), non-Government, private limited company. It was incorporated on March 28, 2013. The Government of India holds 24.5% equity in GSTN and all States of the Indian Union, including NCT of Delhi and Puducherry, and the Empowered Committee of State Finance Ministers (EC), together hold another 24.5%. Balance 51% equity is with non-Government financial institutions. The Company has been set up primarily to provide IT infrastructure and services to the Central and State Governments, tax payers and other stakeholders for the implementation of the Goods and Services Tax (GST). The Authorised Capital of the company is Rs. 10,00,00,000 (Rupees ten crore only).

Strategic Control of the Government.

Several measures of strategic control of Government over GSTN have been envisaged. These are explained below:

Strategic control through Board of Directors (BOD):

The Articles of Association (AOA) of GSTN provide that matters of strategic importance will be decided by the Board of Directors and that the Chairman of the Board will have casting/ second vote where Directors are equally divided over any issue in a Board meeting.

Strategic Control through Special Resolution:

The AOA of GSTN provides that certain matters of strategic importance shall be decided only through Special Resolution (i.e. three-fourth (3/4) of the shareholders voting must vote in favor of such matters). Government's 49% shareholding will ensure that it retains effective control over such matters.

Strategic control through Shareholders Agreement:

An agreement amongst all shareholders of GSTN SPV may provide that till the time Government holds certain threshold of shares in GSTN SPV, specific matters of strategic importance shall not be decided upon without the affirmative vote of the Government.

Placement of personnel on deputation in the GSTN SPV:

Strategic Control is also ensured through deputation of Government officials in the GSTN, at both leadership as well as operational levels. Services Division of GSTN, which is responsible for defining business processes, approving the modules and monitoring the outcomes is managed primarily by Government officers drawn from Central and State Tax Departments. GSTN has two officers of CBEC, eight officers from State Commercial Tax Departments, one officer of Indian Audit and Accounts Service and one officer from the central government working on deputation. Some more officers are likely to join in future.

Agreements between Government and GSTN SPV:

Control over strategic matters could be exercised by Government by incorporating suitable provisions in the Agreement governing service delivery to be executed between Government and GSTN.

Relationship of GSTN with Tax Administrators.

The common GST Portal developed by GSTN will function as the front-end of the overall GST IT eco-system. The IT systems of CBEC and State Tax Departments will function as back-ends that would handle tax administration functions such as registration approval, assessment, audit, adjudication, etc. Nine States and CBEC are developing their backend systems themselves. GSTN is doing the backend for 20 States and 5 UTs. GSTN has been interacting with CBEC and States for ensuring mutual interaction between the front-end that would be operated by GSTN and the back-ends of the tax administrations. Till September 2016, ten workshops have been conducted with the States/CBEC. GSTN will undertake training of tax officials in GST IT system from December 2016 onwards. During the operation phase as well GSTN will continue the interaction with CBEC and states and extend help wherever necessary.

Section 3 - Service offerings

GST Service Providers

The Goods and Services Tax constitutional amendment having been promulgated by the Govt of India, the rollout of the GST Bill will be a collective effort of the Central and State Governments, the tax payers and the IT platform provider i.e. GSTN, CBEC and State Tax Departments. Besides these main participants, there are going to be other stakeholders e.g. Central and States tax authorities, RBI, the Banks, the tax professionals (tax return preparers, Chartered Accountants, Tax Advocates, STPs, etc.), financial services providing companies like ERP companies and Tax Accounting Software Providers, etc.

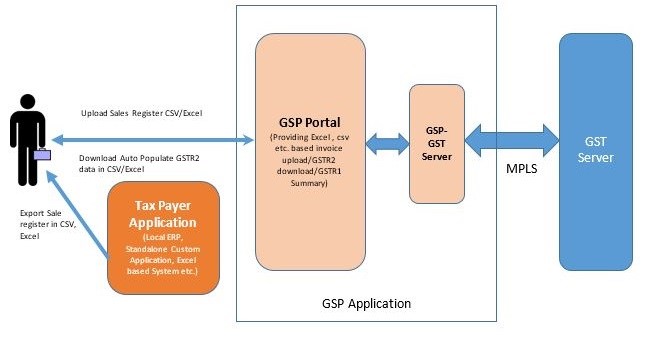

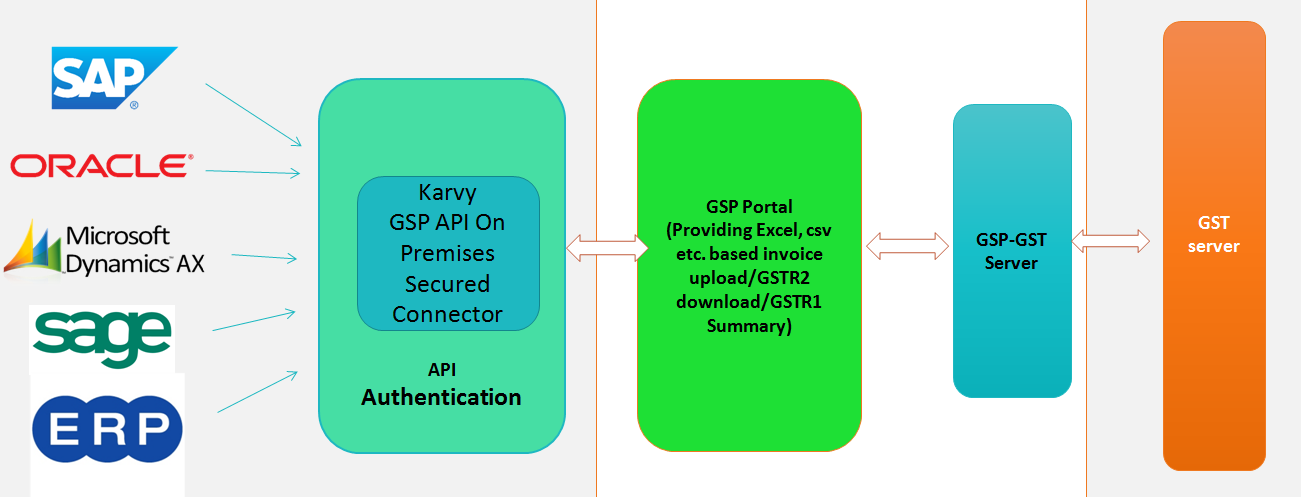

The GST System is going to have a G2B portal for taxpayers to access the GST Systems. However, that would not be the only way for interacting with the GST system, as the taxpayer via his choice of third party applications, which will provide all user interfaces and convenience via desktop, mobile, other interfaces, will be able to interact with the GST system. The third party applications will connect with GST system via secure GST System APIs. All such applications are expected to be developed by third party service providers who have been given a generic name, GST Suvidha Provider or GSP. The GSPs are envisaged to provide innovative and convenient methods to taxpayers and other stakeholders in interacting with the GST Systems from registration of entity to uploading of invoice details to filing of returns. Thus there will be two sets of interactions, one between the App user and the GSP and the second between the GSP and the GST System. It is envisaged that App provider and GSP could be the same entity. Another version could where data, in the required format directly goes to GSP-GST Server. The diagram below gives the most generic case.

In the evolving environment of the new GST regime, it is envisioned that the GST Suvidha Providers (GSP) concept is going to play a very important and strategic role. It is the endeavor of GSTN to build the GSP eco system, ensure its success by putting in place an open, transparent and participative framework for capable and motivated enterprises and entrepreneurs.

GST Compliance requirement by the taxpayer

The taxpayer under GST Regime will have to provide following information at regular intervals:

- Invoice data upload (B2B and large value B2C)

- Upload GSTR-1 (return containing supply data) which will be created based on invoice data and some other data provided by the taxpayer.

- Download data on inward supplies (receipts or purchase) in the form of Draft GSTR-2 from GST Portal created by the Portal based on GSTR-1 filed by corresponding suppliers.

- Do matching of purchases made and that downloaded from GST portal. Finalize the same based on his own purchase (inward supply data) and upload GSTR-2

- File GSTR-3 created by GST Portal based on GSTR-1 and 2 and other info and tax paid.

- Similarly, there are other returns for other categories of taxpayers like casual taxpayer or composition taxpayers.

The GSP Concept

It is expected that the GSPs shall provide the tax payers with all services mentioned above in addition to maintaining their individual business ledgers (sales ledger and purchase ledger) and other value added services around the same. Another important service expected from GSPs is the automatic reconciliation of purchase made and entered in the purchase register and data downloaded in the form of GSTR-2 from the GST portal. In addition, there will be sector-specific or trade specific needs which the GSPs are expected to fulfill. The conceptual diagram depicting the same is as given below.

While the GST System will have a G2B portal for taxpayers to access the GST System, there will be a wide variety of tax payers (SME, Large Enterprise, Small retail vendor etc.) who will require different kind of facilities like converting their purchase/sales register data into GST compliant format, integration of their Accounting Packages/ERP with GST System. Similarly, the specific needs of an industry or trade could be met by GSP. In short, the GSP can help the taxpayers in GST compliance through their innovative Solutions.

GSP Implementation Framework

Tax payer's convenience will be a key in success of GST regime. The tax payer should have a choice to use third party applications which can provide varied interfaces on desktops, laptops, and mobiles and can connect with GST System. The GSP developed apps will connect with the GST system via secure GST system APIs. The majority of GST system functionalities related to taxpayer's GST compliance requirements shall be available to the GSP through APIs. GSPs may use GST APIs and enrich and enhance the tax payer's experience. (The APIs of GST System are RESTful, JSON-based and stateless). GST System will not be available over the Internet for security reasons.

The production API end points can only be consumed via MPLS lines. All APIs will be accessed over HTTPS protocol. The benefits of API based integration are:

- Consumption across technologies and platforms (mobile, tablets, desktops, etc.) based on the individual requirements

- Automated upload and download of data

- Ability to adapt to changing taxation and other business rules and end user usage models.

- Integration with customer software (ERP, Accounting systems) that tax payers and others are already using for their day to day activities

GSTN Ecosystem

Why KARVY

Karvy is a leading player in the financial services industry in India. Spanning over a period of over 3 decades, we have established credentials in multiple business lines, cutting across Corporate registry, Mutual fund registry, Stock broking, Depository services, Commodities, Realty division, Personal advisory services, E-governance services including System Integration, PAN application processing in partnership with NSDL, Biometric enrollment services under UID & NPR, Economic surveys, BFSI services and Telecom services. We have also been recently awarded the certificate of registration as a KYC Registration Agency by the SEBI and to act as an Insurance Repository by the IRDA and as an e-KYC agency by the UIDAI. Given our wide reach and presence, Karvy is among the few corporates in India to be part of market/near market infrastructure across disparate business lines.

Endowed with a well-trained team of 25,000+ employees, our offices are replete with state of the art infrastructure across our 560+ branch networks across 296 cities/towns. Our client service delivery model is uniquely positioned to offer a 360 degree Solution encompassing Technology, People and Infrastructure across the value delivery chain to offer custom built Solutions with precision and scale. We would like to use this opportunity to say that the technology backbone at Karvy is completely managed in-house with over 500 seasoned professionals onboard.

Karvy as a GSP has all that it takes to serve its clients – Service, Technology, and Experience in handling both the corporates as well as a large number of retailers.

Proposed Solution

KARVY’s proposed GSP/ASP Solution for Tax Payers is explained in detail below.

System Architecture

KARVY proposes to use a robust and highly scalable web-based enterprise Solution architecture, conforming to open standards that serve as a unique platform for GSP/ASP Solution to perform the GSP operations and serve the needs of the various Tax Payers.

By keeping in mind, the desire of taxpayers to provide an integrated web based Solution will be achieved through the proposed robust and efficient Solution architecture. The architecture will cater the needs of all the stakeholders seamlessly as part of the GSTR filing.

The proposed Solution will comprise an n-tier architecture that includes a clear separation of presentation, business and data layers. The presentation tier uses a model-view-controller (MVC) framework that always for efficient code reuse as well provides for a clear separation of concerns. The business layer encapsulates the GSTN specific business logic and workflow rules. The business tier architecture is designed to make it very easy to expose any business service as a public API (Application Programming Interface) for consumption by external applications. The data tier provides a highly scalable architecture for data retrieval and storage in a relational database in a standard format.

An industry standard Universal Data Model will be used to store all application related data. This flexible data model is designed to provide a highly normalized database design that allows for efficient data storage as well as enforcing data integrity across all application modules. The extensible data model design will also make it easy to add new components and other additional requirements of the GSTN.

Following diagrams depict the proposed GSP/ASP Solution with high-level business components in the proposed MVC n-tier Architecture.

GSP Application System Architecture

Our Application Service Provider (ASP)

For GSP/ASP Solution KARVY proposes an innovative multi-tenant architecture which allows for computing resources and application code to be generally shared between all the tenants but each tenant has its own data and configuration that remains logically isolated from data that belongs to all other tenants. A metadata layer correctly associates each tenant with the correct database and database security prevents any tenant from accessing other tenants’ data. This Solution has the following major benefits:

- Reduction in the application implementation and maintenance efforts

- Efficient usage of available computing resources

- Enforcement of uniform business processes across the multiple tenants

This multi-tenant architecture can be taken advantage of by adopting this for GSP/ASP Solution for which each module is considered as a universal Logical builder (ULB) and can talk to each other In this architecture each ULB will get its own data and configuration to cater to its specific needs. For example, GSP/ASP Solution proposed dashboard module can aggregate all the ULBs like data using the multi-tenancy Solution and for overall monitoring and generate the analytics on top of it.

Features

- Interface for GSTR1

- Interface for GSTR2 download

- Interface for confirmation of credits for GSTR 2

- Interface for Auto reversals, adjustments, etc.

- Auto population of GSTR 3

- Workflow capability

- Authorization ( Maker/Checker) for confirmation of returns.

- Role based Authorization for confirmation of various returns

- Dashboard reporting – Output Tax, Credits available, credits claimed, reversal, tax paid, etc. with drill down capability

- Ability to view multiple GSTN Registrations in single ID based on the authorization

- Ability to download data in spreadsheets

- Ability to file all required GSTR4 to GSTR11

Value Added Services

- Comparison of GSTR2 data vs. Purchases booked in ERP

- Ability to auto reconcile and identify open items

- Auto classify open items based on the type of mismatch

- Reports & Dashboard for open items, matched data, available credits, reversals, etc.

- Vendor Management – Mechanism in place to follow up with the vendors of our clients for mismatched cases on the specific authorisation by the client.

Connector Magic XPA Integration Features

- Large library of more than 80 pre-built components and customizable connectors and adaptors

- Open, standards-based development framework enables connection to all databases, platforms, and file formats

- A comprehensive, enterprise-grade studio enables both developers and analysts to rapidly develop and deploy integration flows

- Support for business process management (BPM) life cycle optimization to improve organizational efficiency and performance

- User-friendly, step-by-step wizards simplify integration

- Business Flow Editor provides drag-and-drop functionality for easy configuration of business processes

- Single portal for unified access to business information

- Visual Data Mapper transforms information regardless of format

- Automated handling of exceptions and errors in business processes

- Simple and intuitive modeling environment and graphical user interface

- Powerful built-in security and encryption tools

- Online performance monitoring and alerts

- Logging, recovery, inter-system messaging and routing services

- Simulation tool enables project scenario testing before full-scale implementation

- Easily scalable from functional collaboration to company and enterprise workflows

- Out-of-the-box SOA for any organizational scale

- Certified and Gold SAP Software Solution partner

- Gold Partner of Oracle and certified by Oracle for JD Edwards E1 and The World

- Certified for Salesforce and official AppExchange Partner

- Member of the Microsoft SharePoint Integration Forum

Non-Functional Features

- Security: The Solution provides an end-to-end security model that protects applications, services, data from malicious attacks or theft from both external and internal users. Also, the Solution provides fine grained authorization and access control mechanisms to ensure that sensitive and confidential information is not accessible to non-authorized persons.

- Performance: Performance is a prime requirement of the proposed Solution. There are many factors that may affect the performance, two important ones being webpage/Report/ content volume and retrieval response time. Under the proposed system all processes will be executed online through a portal based application with the necessary start of the art hardware and software configuration.

- Availability: All the modules and the application must be available 24/7.

- Scalability: The architecture should be proven to be highly scalable and capable of delivering high-performance as and when the data volumes increase. It is required that the hardware, software, network and application and deployment architecture should provide for Scale-Up and Scale out on the Application and Web Servers, Database Servers, Application Servers, and all other Solution components.

- Backup and Recovery: It is required to implement the Storage Solution to address the Data backup/storage and retrieval requirements of the GSP/ASP Solution.

- Extension/Flexibility: System will be developed using Industry Standard MVC Architecture which allows Extensibility/Flexibility encompasses the ease of extending the architecture to include new business functions and technologies in the future.

- Usability: The application should be easy to use with minimum learning by end users.

- Portability: The proposed system facilitates the coexistence and inter-changeability of multiple hardware and software technologies, tools, protocols, and interfaces.

Design Principals

The Proposed Application Software is designed to adhere it to follow the design principles based on Next Generation N- tier architecture and Framework and supports the deployment of an end to end Solution for the Client.

The various Systems and Sub-Systems that form part of this Solution platform are modular seamlessly integrated and are scalable for future upgradeability to deliver the overall functionality.

The Platform architecture support load balancing and is highly scalable to support an increase in load – increase in transactions, customers, increase in data and documents storage and increase in web users.

The Software architecture is designed to supports scale and availability. Every component is designed to scale to large volumes and support Millions of transaction and records. The Architecture is designed for high availability to accommodate failure and design for recovery. It is based on a Modular Architecture so that it can be integrated with multiple applications based on a concept of service through APIs. The various services and applications that consume the service are integrated through a SOA Layer.

The proposed Solution integrates existing internal and external modules/applications through the Multiple APIs/Interfaces and gives the Unified framework with a uniform workflow system so that it provides a common operating workflow Solution for the real estate services. The various components that can be integrated cover – core modules, front end and backend systems and external service providers like GSTN, BANKS, CBEC and others.

Highlights

- N-Tier model is the framework in which application user interface, logic, data, and their associated processing and repair, are separated from each other in a logical manner.

- Horizontal scalability as an open scale out by addition of Servers in the active-active configuration for varying loads and to support load balancing architecture.

- Highly available with no single point of failure across the servers, sites, and services.

- Distributed data store and distributed computing using Hardware.

- Use of right data store for right purpose

- Asynchronous processing throughout the system allowing loose coupling of the various components and supporting independent component level scaling.

The Design principle and consideration are compliant to the General and Design Consideration Guidelines as specified by GSTN and the compliance is provided for the same.

- Prevention of unauthorized access.

- Accessible only after approval from application owner and the competent authorities.

- Secured Data Transfer through SSL and necessary data encryption

- The access should be on a role basis rather than universal

- The access control system will cover:

- Identification

- Authentication

- Authorization and Access Control

- Administration

- Audit

Infrastructure Deployment

Following is the logical view of the Infrastructure deployed at the Data Centre to configure and run the proposed GSP/ASP Solution.

General Enterprise Requirements

Data Security and Privacy

We would be using the Microsoft Azure cloud to host the GSP & ASP application. Following is extracted from Microsoft Azure’s data protection and privacy policy.

Azure allows customers to encrypt data and manage keys and safeguards customer data for applications, platform, system and storage using three specific methods: encryption, segregation, and destruction.

Data isolation. Azure is a multi-tenant service, meaning that multiple customers’ deployments and virtual machines are stored on the same physical hardware.

Protecting data at rest. Azure offers a wide range of encryption capabilities, giving customers the flexibility to choose the solution that best meets their needs. Azure

Key Vault helps customers easily and cost effectively streamline key management and maintain control of keys used by cloud applications and services to encrypt data.

Protecting data in transit. For data in transit, customers can enable encryption for traffic between their own VMs and end users. Azure protects data in transit, such as between two virtual networks. Azure uses industry standard transport protocols such as TLS between devices and Microsoft data centers, and within data centers themselves.

Encryption. Customers can encrypt data in storage and in transit to align with best practices for protecting confidentiality and data integrity. For data in transit, Azure uses industry-standard transport protocols between devices and Microsoft data centers and within data centers themselves. You can enable encryption for traffic between your own virtual machines and end users.

Data redundancy. Customers may opt for in-country storage for compliance or latency considerations or out-of-country storage for security or disaster recovery purposes. Data may be replicated within a selected geographic area for redundancy.

Data destruction. When customers delete data or leave Azure, Microsoft follows strict standards for overwriting storage resources before reuse. As part of our agreements for cloud services such as Azure Storage, Azure VMs, and Azure Active

Directory, we contractually commit to specific processes for the deletion of data.

Multi-Factor Authentication. Microsoft Azure provides Multi-Factor Authentication (MFA). This helps safeguard access to data and applications and enables regulatory compliance while meeting user demand for a simple sign-in process for both on premises and cloud applications. It delivers strong authentication via a range of easy verification options—phone call, text message, or mobile app notification—allowing users to choose the method they prefer.

Access monitoring and logging. Security reports are used to monitor access patterns and to proactively identify and mitigate potential threats. Microsoft administrative operations, including system access, are logged to provide an audit trail if unauthorized or accidental changes are made. Customers can turn on additional access monitoring functionality in Azure and use third-party monitoring tools to detect additional threats. Customers can request reports from Microsoft that provide information about user access to their environments.

Privacy

Restricted access by Microsoft personnel. Access to customer data by Microsoft personnel is restricted. Customer data is only accessed when necessary to support the customer’s use of Azure. This may include troubleshooting aimed at preventing, detecting, or repairing problems affecting the operation of Azure and the improvement of features that involve the detection of, and protection against, emerging and evolving threats to the user (such as malware or spam). When granted, access is controlled and logged. Strong authentication, including the use of multifactor authentication, helps limit access to authorized personnel only. Access is revoked as soon as it is no longer needed.

Notification of lawful requests for information. Microsoft believes that customers should control their data whether stored on their premises or in a cloud service. We will not disclose Azure customer data to law enforcement except as a customer directs or where required by law. When governments make a lawful demand for Azure customer data from Microsoft, we strive to be principled, limited in what we disclose, and committed to transparency.

Microsoft does not provide any third party with direct or unfettered access to customer data. Microsoft only releases specific data mandated by the relevant legal demand.

If a government wants customer data—including for national security purposes—it needs to follow the applicable legal process, meaning it must serve us with a warrant or court order for content or subpoena for account information. If compelled to disclose customer data, we will promptly notify the customer and provide a copy of the demand unless legally prohibited from doing so.

Technical Details

- The application will have a latency of less than 1 second measured on the same network.

- The connector will be an on premise application whereas the Dashboard, Returns upload, Notifications, etc. will be a cloud based application.

- We will not be storing any data on our servers. However, the logs of each activity will be maintained on the GSP server for future references.

Scope of Work GSP Services

- Karvy as the GSP will provide continuous and flawless Services at all times unless it is prevented by reason of any Force Majeure Event or any other exceptions as may be set out under the SLA as defined by GSTN.

- Karvy as the GSP shall add and reflect, on its GSP Application, such disclaimers as GSTN may require from time to time.

- Karvy as the GSP shall ensure that GSP Application is connected to GST System in a continuous asynchronous mode whenever the GSP has to provide any kind of Services to the Taxpayer.

- All the APIs provided by GSTN to Karvy as the GSP shall be further released to its service providers in the same form and quantum as may be provided to it by GSTN. The GSP shall not discriminate or show bias or give preferential treatment, directly or indirectly, in sharing of the APIs above.

- Karvy as the GSP shall generate sub-license key for its ASP for authenticating to the GSTN server and for encryption and decryption of the data from and to the GSTN server.

- Karvy as the GSP shall connect to GST system through MPLS API consumption to be measured at GSP and GST end to assess usage for billing purpose.

- All ASP’s of Karvy as the GSP shall connect to and aggregate to GSTN through our API’s.

- Karvy as the GSP will offer additional value added services like bulk upload of invoices, conversion of invoice data format like csv, xls, txt to Json format, prepare GSTR’s with validation through our API’s.

- Karvy as the GSP will comply with data privacy, encryption, authorization features provided by GSTN.

- Karvy as the GSP will ensure security, privacy, and integrity of data traveling from end user application to its system and GSTN.

- Karvy as the GSP will provide short as well long duration session to their customers (GSTN provides both facilities) based on user preference.

- Karvy as the GSP shall maintain audit as well as transaction logs of all the request/response processed by it for a period of 7 years by capturing the complete meta data available in HTTP headers, request and response time stamp along with status (success/failure/timeout etc.), requesting third party details like application id /license /sub-license key, API type etc. as prescribed by GSTN from time to time.

- Karvy as the GSP understands and agrees that the logs maintained by it shall be shared with any individual or entity only on a need basis and that the storage of the logs maintained by it shall comply with all the relevant laws, rules and regulations.

Standard Services for KARVY ASP –

Karvy ASP application will provide below services-

Returns, Records, and Reconciliation-

- GSTR - 1 (Returns for Outward Supplies)

- GSTR - 2 (Returns for Inward Supplies)

- GSTR 1A, 2A – Reconciliation Coordination

- GSTR - 3 (Monthly Return)

- GSTR – 4 (Quarterly return for registered persons opting composition levy)

- GSTR – 5 (Return for Non-Resident Taxable Persons)

- GSTR - 6 (Return for ISD) including calculation of turnover and credit distribution

- GSTR - 7 (Return for Tax Deducted at Source)

- GSTR – 8 (Statement for Tax Collection at Source)

- GSTR - 9 (Annual Return)

- Reverse charge calculation including generation of self-invoice

- Maintenance of Tax Liability, Cash Payments, and Input Tax Credit ledger

Remote Training and Handholding sessions

Implementation Methodology

- Configuration Validation:

- Requirements Validation at the Customer Site

- Hot Staging of the Solution

- Installation, Testing and Go Live of the Solution

End User Training Approach and Methodology

The Training Specialist will train key operational staff in the use of the system. This training will be oriented towards the usage of the system as defined by the business requirements and will employ a hands-on method of teaching using the customer’s system. At the Conclusion of the training, the customer will sign a Training Verification Checklist. A Concluding meeting will be conducted with the customer. The purpose of the meeting is to Review the activities of both the installation and the training and to provide the customer with the necessary information related to both the Limited Remote Consulting and the Customer Service Support.

Support Services

- Helpdesk Number to access Support

- Urgent business-critical issues handled

- Remote access tools used by support to address your issues allow specialists to directly connect to your computer

- Escalation to Development, when needed

- General usage questions answered

Support Methodology

- Ticketing system – helps to track customer inquiries

- Urgency Codes based on the criticality of support requests:

- Critical - Needs immediate attention—cannot do any work without a resolution.

- Business affected.

- Severe - Problem impacts work, but does not stop business

- Standard - Problem encountered, but system operational and business continuing.

- Low - System not affected, respond when able/request for information.

Knowledge transfer Methodology

- Documentation of the customization

- Documentation of the API’s

- Training on the connector

- Training on the application landscape and usage

Post Go Live Support

- AMC for Magic Connector

- AMC for GSP services